LYNN BERGMAN: “TAX THE RICH” DISPELLED EIGHT DECADES AGO!

“Tax the Rich” Dispelled Eight Decades Ago!

Andrew Mellon’s Tax Cuts Fueled The Roaring 20’s; Hoover and Roosevelt’s Taxation Binge Spawned The Great Depression.

A book review by Lynn Bergman

I finally caught up on my reading and ordered three great books; “The Myth of the Robber Barons”, “New Deal or Raw Deal”, and “FDR Goes to War”, all by Burton W. Folsom Jr. who is a professor of history and management at Hillsdale College in Michigan. Folsom has written numerous books and countless journal columns.

Chapter 6 of “The Myth of the Robber Barons” recounts the taxation experiments of Andrew Mellon. Mellon’s grandfather fled Ulster, Ireland in 1818 to escape the high taxes of the Napoleonic Wars. Mellon’s father was taught to avoid debt, be honest, and work hard. Young Andrew learned about supply and demand at age nine by selling apples from the family orchard and assisted his father in business tasks as a teenager.

After his father retired early he and his brother ran the family banking business. Andrew invested heavily in Alcoa Aluminum and Gulf Oil in the early 1900s. His venture capitalism made him almost a billionaire by 1920, along with John D Rockefeller (Standard Oil) and Henry Ford.

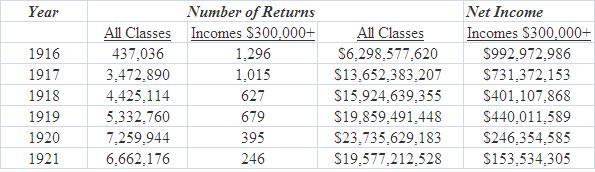

After World War I, the winner of the 1920 presidential election, Republican Warren G. Harding, asked 65 year old Andrew Mellon to be his Secretary of the Treasury to revive a stagnant economy, a rising national debt, and a crushing federal tax burden… resulting from the war and its 77% maximum income tax rate. The decline in wealth that was essentially confiscated in order to win the war is shown in the table below:

Table 1: The Decline of Taxable Incomes Exceeding $300,000 from 1916 to 1921

Summarizing, during the period surrounding World War I, the maximum income tax rate rose to 77%, the number of citizens earning an income over $300,000 fell by over 80%, their income fell by 85%, and the national debt increased 16 fold from $1.5 Billion in 1916 to $24 Billion in 1919. Secretary of the Treasury Andrew Mellon had his work cut out for him. Fortunately, his experience as a venture capitalist would serve him well in reviving the stagnant post-war economy.

But first, we must put Mellon’s proposals and subsequent success with revenue maximization in context by recounting the history of the income tax.

Brief History of the Income Tax

The first income tax of 3% on income over $800 had been assessed during the Civil War, was raised twice, but was repealed in 1872 after the war ended. Congress, in 1894, passed a flat 2% tax on income over $4,000 but the Supreme Court declared it unconstitutional.

In 1913, progressive proponents of an increased role for the federal government from Wisconsin, Nebraska and Michigan led the effort to pass the sixteenth amendment creating the first peace time income tax, as follows:

In 1916, Congress hiked the tax to a range of 2% to 15% (on incomes over $2 Million) and also assessed the first inheritance tax at 5% (Founder Thomas Paine had suggested a 10% estate tax to fund modest subsidies for those entering adulthood and for extreme old age security).

During World War I, the income tax ranged from 4% to a near confiscatory 77%. As a result, incomes over $300,000 fell from 1,296 taxpayers reporting a total income of $992,972,986 in 1916 to 246 taxpayers reporting a total income of $153,534,305 in 1921. Meanwhile, the inheritance tax was increased from 5% to 25% by the time Mellon took office and was raised to 40% at the same time his plan was released in 1924. During the World War and afterwards, high taxation had chased capital out of productive investment. To avoid the confiscation, the wealthy invested their assets into tax exempt municipal bonds.

Municipal bonds (that yielded about 5%) spurred the construction of municipal infrastructure, but starved the nations industries. While cities built football stadiums and civic centers, the number of factory jobs declined due to the lack of venture capital. For example, in 1923 when William Rockefeller, the brother of John D. Rockefeller, died, he owned $44 Million in tax exempt bonds and only $7 Million in Standard Oil stock.

“Taxation: The People’s Business”

When Mellon arrived in Washington in 1920, the top tax rate was 73%. As Treasury Secretary, and after carefully collecting and studying economic data, Mellon concluded “High taxes are the chief parasites draining the lifeblood of the American economy”. He suggested that lower taxation rates at all levels of income would result in significantly more productive investment and subsequent increases in revenues. Mellon, of course, realized that there was a limit to which tax rates could be lowered while still increasing revenues. The problem was to optimize the rates to maximize revenues.

Mellon’s book, “Taxation: The People’s Business”, published in 1924, along with his reputation of “Financier of the Universe” eventually resulted in full presidential support for his recommendations. Mellon quietly convinced Harding, then Coolidge. Harding died in 1923, but Coolidge and Mellon found closeness in both personality and philosophy that made them very effective proponents of the “Mellon Plan”.

Mellon understood that there was a limit on how much income taxes could be cut while maintaining revenue increases. He believed that 25% was about as much as wealthy people would pay in income taxes before they rushed to tax shelters such as municipal bonds. Mellon’s four point plan was as follows:

- Cut the top income tax rate to 25%

- Cut taxes on low incomes

- Reduce the federal estate tax (Mellon believed that states should levy estate taxes)

- Efficiency in government

Mellon practiced what he preached; during the 1920s, he cut an average of one staff person a day from the Treasury Department as part 4 of his plan called for reducing the federal budget from $18 Billion in 1919 to his target of under $4 Billion by 1930.

The 1924 elections shifted the balance of power to the conservatives. Tax cuts had been the major campaign issue and Republicans had the white house and large majorities in both houses of congress, so most of the Mellon Plan was passed in 1926. The results of the 1926 tax cuts are shown below:

Table 2: The Tax Revenue Collected According to Income Groupings Before and After the 1926 Tax Cuts

The trend continued with smaller tax cuts in 1928 and 1929. In 1929, total income tax revenues exceeded $1 Billion with those earning over $100,000 paying 65% of the total and those earning under $10,000 paying 1.3% of the total.

Progressives could not argue with the resulting revenue increases so they instead challenged Mellon’s motives. A “Board of Tax Appeals” had awarded $3.5 Billion in refunds as well as $5.3 Billion in added assessments during the 1920s, resulting in a net increase in revenue of $1.8 Billion from the actions of the appeals board. Progressives “cherry picked” the appeals board’s results and tried to attack Mellon’s integrity but complete analysis of the data revealed that prominent Democrats and Republicans were among both the winners and losers in tax cases during the 1920s.

Changes in Tax Policy - 1920 to 1930

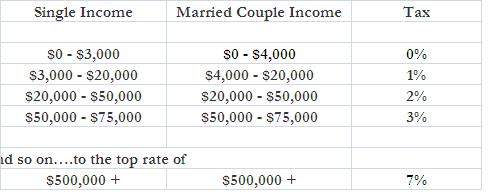

The personal income tax “floor” began the decade at 4% for single income earnings up to $3,000 and married couple earnings up to $4,000 and ended the decade at 0.5%. The top income tax rate in 1920 was 73%, which was lowered to 58% in 1921, 46% by 1924, and 24% by 1930.

The corporate tax that had risen to 18% during the war was 10% when Mellon took office, and was raised to 12.5% in 1924.

The federal inheritance tax in 1920 was 25% on estates over $50,000 and was raised to 40% in 1924, but was finally lowered in 1928 and 1929 to 20%.

Because the inheritance tax had been so high during the 1920s, the wealthy began gifting their wealth to heirs, which prompted the passage of a gift tax in 1924. Subsequently, the wealthy shifted their fortunes into tax-exempt foundations, many of which endure today.

Mellon also convinced political power brokers to slash excise taxes during the decade, a sincere attempt to make life better for the lower income earners that are the hardest hit by such taxes.

The Dirty Thirties

Mellon stayed on under President Herbert Hoover but resigned in February, 1932. Franklin Roosevelt took office in 1933 with his promise of a “New Deal”. Under both Hoover and Roosevelt, the top rate for income taxes was increased to 63% after 1932 and to 79% after 1934. Investors again sheltered their investments to avoid income and estate taxes, triggering a plethora of new excise taxes to maintain the federal revenue stream.

From 1929 to 1935, federal revenue from personal income taxes declined from $1,095 Million ($1.095 Billion) to $527 Million ($0.527 Billion). During the same time frame, excise tax revenues shot up from $539 Million to $1.363 Million, draining the last few drops of fuel from the American Economic Engine of Prosperity.

Commentary

After excessive taxation of all tax venues forced venture capital into municipal bonds immediately following the war, and after increased estate taxes further drove venture capital into tax exempt foundations during the roaring twenties, it was probably the extensive excise taxes of the early thirties that put the final nails into the coffin of the Industrial Revolution, spawning The Great Depression.

Postscript:

Author Folsom points out that tax records have been available for almost sixty years. Studies of tax records by Roy and Gladys Blakely, Benjamin Rader, James Gwartney, and Thomas Silver have been available for some time. Yet there seems to be almost no correct information in any college history text on the impact of Mellon’s tax cuts or on the New Deal tax hikes.

The false assumptions presented by authors John M. Blum of Yale, William S. McFeely of the University of Georgia, Edmund S. Morgan of Yale, Arthur Schlesinger, Jr. of the City University of New York, Kenneth Stampp of Berkeley, C. Van Woodward of Yale, John Garraty of Columbia University, Thomas A. Bailey & David M. Kennedy of Stanford, and Pulitzer Prize winning economic historian, Irwin Unger are revealed in Folsom’s book. Many of the false assumptions are ensconced in school textbooks these authors have written! As Folsom puts it so succinctly, “Expertise in the field, in fact, does not seem to correlate with presenting accurate information.”

Finally, at the end of Chapter Six, Folsom points out that…

“Andrew Mellon never made an investment without knowing the relevant facts; his business success demonstrated his grasp of financial situations. In similar fashion, modern politicians, businessmen, and historians would do well to learn the facts of American tax history before they try to plot its future.”

© 2012 Lynn A. Bergman

DakotaBeacon

DakotaBeacon